We pulled real Google search data for 35 jewelry and watch brands and ranked them by how much branded demand actually moved over the past year. One headline stands out: the direct-to-consumer search story everyone keeps repeating has cooled.

Branded search volume is the cleanest read on momentum we have. When someone types a brand name into Google, they already want that brand. They are looking to buy it, compare it, or learn more. That is demand you can measure, not sentiment you have to guess at.

Some of what we found confirms the obvious. A lot of it does not.

How We Measured It

The numbers come from Google Keyword Planner, United States, for the twelve months through April 2026. Growth is the most recent quarter, February through April 2026, measured against the year-ago quarter, May through July 2025. We compare those two windows on purpose, because both sit outside the December gift-shopping spike. A straight quarter-over-quarter read would make almost every brand look like it is collapsing in the new year, and that is seasonality, not decline.

We set a floor of 3,000 monthly searches so the ranking reflects real demand instead of statistical noise. Google reports volume in rounded bands, so treat small month-to-month moves as directional. Full methodology is at the bottom.

This is the first quarterly edition, so it sets the baseline. The up-and-down position movement quarter to quarter starts with the next update.

The Q2 2026 Ranking

Every brand that clears 3,000 monthly branded searches, ranked by year-over-year change:

Q2 2026 — Fastest-Growing Brands

Branded Google search volume, US · data through April 2026 · sort any column

| # | Brand▼ | Tier▼ | Searches/mo▼ | YoY▼ | Trend | Move |

|---|---|---|---|---|---|---|

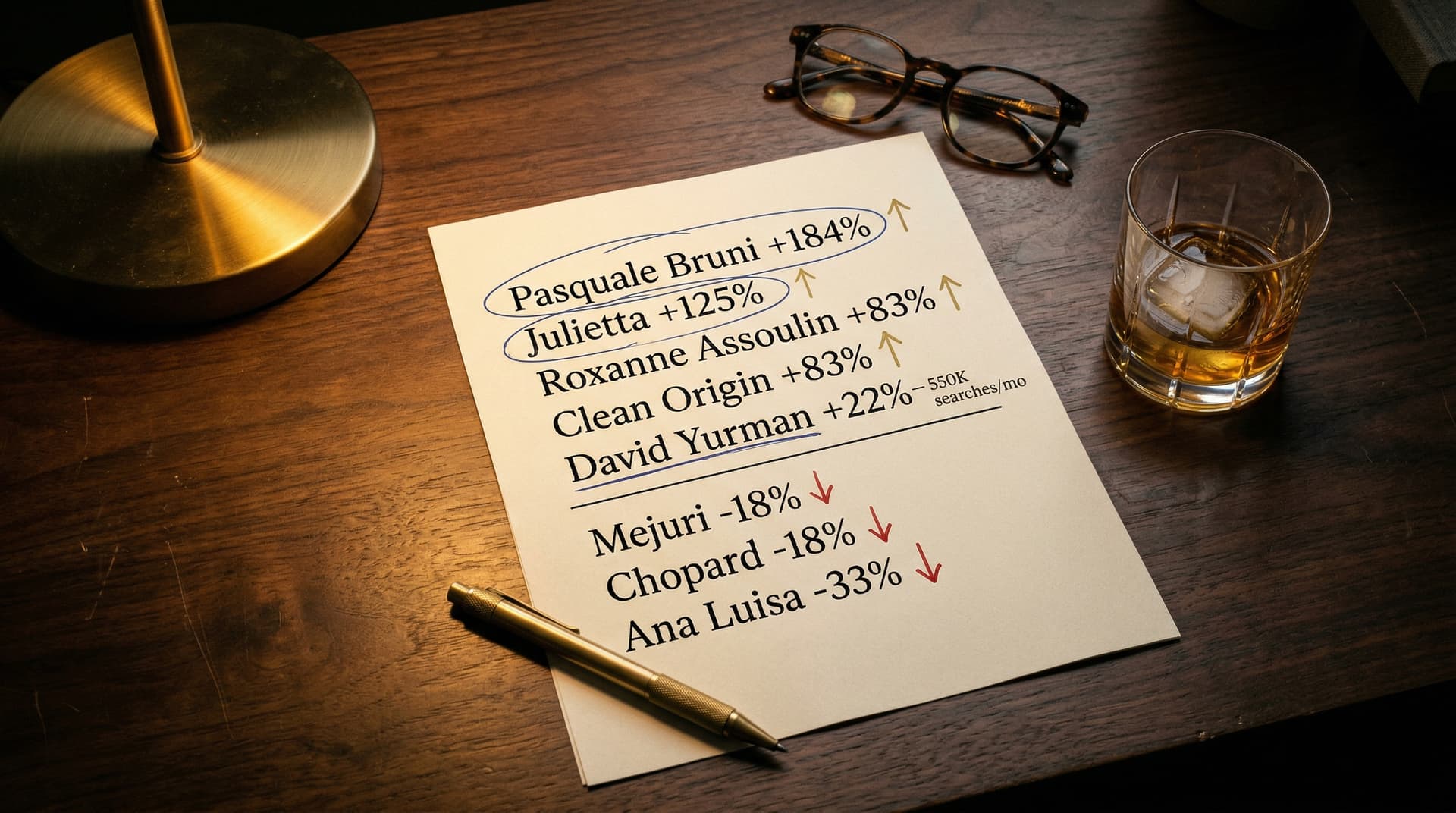

| 1 | Pasquale Bruni† | High-end | 3,600 | ▲+110% | new | |

| 2 | Bucherer | High-end | 13,900 | ▲+31% | new | |

| 3 | Clean Origin | Mid | 5,600 | ▲+25% | new | |

| 4 | Tacori | Mid | 9,900 | ▲+22% | new | |

| 5 | Graff | High-end | 3,100 | ▲+22% | new | |

| 6 | Piaget | Heritage | 33,100 | ▲+20% | new | |

| 7 | Alex Moss NY | High-end | 5,900 | ▲+16% | new | |

| 8 | Buccellati | Heritage | 20,800 | ▲+15% | new | |

| 9 | Catbird | Entry | 19,500 | ▲+8% | new | |

| 10 | Roxanne Assoulin | Entry | 14,800 | ▲+6% | new | |

| 11 | Messika | High-end | 18,100 | ▲+6% | new | |

| 12 | Bario Neal | Entry | 4,400 | ·0% | new | |

| 13 | David Yurman | Mid | 483,300 | ·0% | new | |

| 14 | Mikimoto | High-end | 25,500 | ·0% | new | |

| 15 | Tiffany & Co. | Heritage | 591,000 | ·0% | new | |

| 16 | Cartier | Heritage | 591,000 | ·0% | new | |

| 17 | Chaumet | Heritage | 10,600 | ·0% | new | |

| 18 | Pomellato | Heritage | 7,100 | ·0% | new | |

| 19 | Ritani | Mid | 12,100 | ▼-1% | new | |

| 20 | Brilliant Earth | Entry | 301,000 | ▼-7% | new | |

| 21 | Chopard | Heritage | 22,200 | ▼-7% | new | |

| 22 | Mejuri | Entry | 231,000 | ▼-13% | new | |

| 23 | Van Cleef & Arpels | Heritage | 8,100 | ▼-13% | new | |

| 24 | Dorsey | Entry | 5,500 | ▼-23% | new |

† Pasquale Bruni: +110% rides one unusually strong month against a small base. Read as volatile, not a durable category leader.

One caveat before you read too much into the top line. Pasquale Bruni's +110% rides one unusually strong month against a small base, so it reads as volatile rather than a genuine category leader. The durable growth sits just below it, with Bucherer, Clean Origin, Tacori, Graff, Piaget, and Buccellati.

What Is Actually Growing

The real movers are not who the trade press would predict.

- Bucherer (+31%, 13,900/mo): the Swiss watch retailer keeps expanding its US footprint, and search is following.

- Clean Origin (+25%, 5,600/mo): the one lab-grown name still climbing while the bigger lab-grown brands flatten out.

- Tacori (+22%, 9,900/mo): heritage bridal that markets hard through its retail partners and photographs well on social.

- Piaget (+21%, 33,100/mo) and Graff (+22%, 3,100/mo): high jewelry houses pulling demand through editorial and celebrity placement.

- Alex Moss New York (+16%, 5,900/mo): custom high jewelry with a sharp holiday gifting spike, proof that a smaller name can still build real branded demand.

- Buccellati (+15%, 20,800/mo) and Messika (+7%, 18,100/mo): European houses gaining US ground through retailer partnerships.

The pattern is hard to miss. Established names with strong retail and editorial muscle are taking share, not the digital-first upstarts.

The DTC Search Story Cooled

This is the part that breaks the script. The brands the internet keeps calling the future of jewelry are flat or shrinking in branded search.

- Mejuri (-13%, 231,000/mo): still one of the largest names here, but demand slid over the year.

- Brilliant Earth (-7%, 301,000/mo): the biggest lab-grown brand, edging down.

- Dorsey (-23%, 5,500/mo) and VRAI (-32%, below the floor): cooling fast.

None of these brands is in trouble. Mejuri and Brilliant Earth still command enormous demand. But the runaway search growth that defined them a few years ago has leveled off. If your plan assumed these names would keep pulling customers up and to the right forever, the data says think again.

The Giants Are Holding, Not Growing

Tiffany at 591,000 monthly searches, Cartier at 591,000, and David Yurman at roughly 483,000 are all flat year over year. Massive demand, no momentum. If you are an authorized dealer for any of them, the customers exist, but the brand is not growing the pie for you. Your marketing has to do that work.

Smaller Names Worth Watching

Below the 3,000 floor, a few brands are rising fast off small bases, so read these as early signals rather than settled trends: Aurate (+25%), Julietta (+25%), and Mondo Mondo (+40%). If any of these sit in your case, the demand is building before most retailers have noticed.

What This Means for Your Store

The market is rewarding brands that pair real-world presence with sharp digital and editorial work. That is a fight independent retailers can win locally.

- If you carry lab-grown diamonds, say so plainly and build pages for "lab-grown engagement rings [your city]." Clean Origin is proof the demand is still there.

- Own the local search for the growing brands you stock. "Tacori engagement rings [your city]" and "Bucherer [your city]" are high-intent and mostly uncontested.

- Do not coast on the flat giants. If you sell Tiffany or Cartier, your job is to be the best local resource for those buyers, because the brand will not hand you growth.

- Watch the risers early. Picking up an Aurate or a Clean Origin before your competitors do is cheaper now than it will be in a year.

Want your own brand lineup run against this data for your market? Talk to us. We will show you where branded demand is heading and how to capture it before the brands capture it for someone else.

Methodology

Data source: Google Keyword Planner, accessed through Google Ads, United States only.

Time period: the trailing twelve months, May 2025 through April 2026, which is the most recent window Keyword Planner reports.

Brands: 35 jewelry and watch brands with a US consumer presence and a trackable branded search term. Ambiguous brand names were queried with a qualifier, for example "graff diamonds" or "dorsey jewelry," to separate brand demand from unrelated searches.

Growth: the most recent quarter, February through April 2026, compared with the year-ago quarter, May through July 2025. Both windows fall outside the December peak, which keeps seasonality from distorting the result. Keyword Planner returns only twelve months, so this is a trailing-year change rather than a strict same-quarter comparison. Once we have a second year of tracked data, future editions will move to a true same-quarter read and add quarter-to-quarter position movement.

Volume floor: brands under 3,000 monthly searches are noted separately, because Google's rounded reporting makes small-volume percentages unreliable.

Limitations: search volume is a demand signal, not a sales figure. A brand with high search and no local presence cannot capture your buyers, and a brand with modest search but strong in-store traffic may look smaller here than it really is. These are momentum indicators, not revenue rankings.